Where We Are Heading

After a whirlwind of a year in 2020, the housing market looks like a minefield of complications. Thanks to COVID-19 and its impact on the U.S., the right decisions for a potential home buyer may be completely different from what they were in 2019.

Some have to permanently work from home from now on, which means you need an office space. Others, first-time home buyers, may have learned they’re only willing to settle down in the suburbs now. Regardless, you are stuck grappling with a seemingly unpredictable market in a recovering economy.

However, housing market indicators can tell us what 2021 will likely hold for potential buyers and sellers. It’s crucial to keep up to date on the real estate market and its changes as you approach buying a house. So, it’s best to inform yourself of the trends that will likely continue to occur over the upcoming year. As a result, you’ll be able to navigate a changing market and lockdown on the best opportunity for you to purchase a new home.

Mortgage Rates

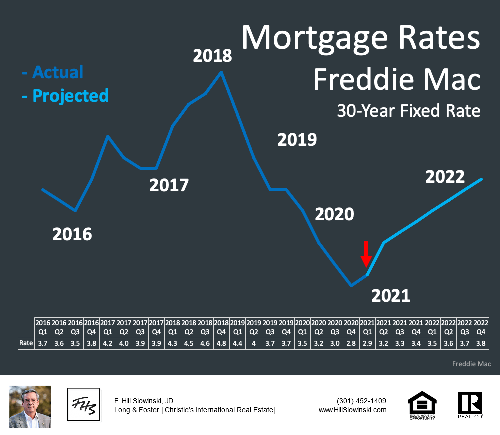

Mortgage rates are coming off of record lows entering 2021, with a 30-year fixed-rate loan’s average having slipped down to 2.66%. Following the new benchmarks, there will be some fluctuation as mortgage rates climb back up to a modest 3% on average. And, according to REALTOR.com, the final average rate is projected to be 3.4% by the end of the year.

Overall, these rates are low because the economy is still in recovery following COVID-19, and they don’t seem to be going anywhere soon. Jerome Powell, the Federal Reserve Chairman, spoke on the interest rates late last year in an NPR interview, saying, “We think that the economy’s going to need low interest rates, which support economic activity, for an extended period of time.”

This is good news for prospective home buyers, especially those concerned about rates rising during the time it would take to close on a house. Generally, closing can take 30 – 45 days. With the mortgage rate stability this upcoming year, it’s likely that you’ll either have a consistent rate throughout the closing period or very close to it. As a result, you may avoid having to pursue a mortgage rate lock. Also called rate protection, a mortgage rate lock best works when interest rates are rapidly changing to help freeze your interest rate while you close. While that provides some protection, it doesn’t allow you to take advantage of an interest rate decrease and may force you to pay your lender a percentage fee if you exceed the lock’s term.

While mortgage rates are unlikely to change drastically or quickly, it’s always good to keep an eye out and plan your close strategically, even if rates are relatively consistent.

Homes May Become Less Affordable

While 2020’s low mortgage rates will continue into 2021 with some reasonable increase, they can only do so much to offset overall housing prices.

Prices were already high last year based on reports from the U.S. Census Bureau. The median U.S. (new) home sales price was $355,900 in December, a difference of $24,500 to 2019’s median of $331,400 at the same time in 2019. Prospective home buyers will find these housing prices aren’t going to drop either. Predictions forecast median sale price appreciation to go up by 5.7%.

Supply and demand contribute to the increase, with suburban properties, particularly those featuring home-office spaces, expected to be in the highest demand. COVID-19 exacerbated the affordable housing issue, but it has been a running concern for investors and potential buyers for years now. However, increased housing prices can be a positive sign for the economy and its growth, encouraged by a competitive market experiencing high demand.

If you’re a first-time home buyer and concerned about covering the down payment in this housing market, down payment assistance may be possible. This assistance typically comes in the form of grants, loans, or other programs. Choosing one ultimately depends on the type of help you require, like whether you’re struggling to purchase a rural home or with closing costs, and your background. For example, there are VA loans for veterans, active Armed Forces members, and certain spouses of deceased service members.

Down payment assistance is a valuable option for struggling first-time home buyers, but they come with requirements to qualify. Make sure to research what credit score and income level you’ll need since they’re the most common ones.

Home Value Growth Is Projected To Continue

That high demand and low supply across the U.S. housing market will also drive continued home value growth into 2021. According to Zillow, home values are expected to increase by 10.3% from November 2020 to November 2021. There is a benefit to this, despite how it makes purchasing harder on buyers. As home value continues to increase, so does its resale value, which is important for current homeowners.

When home value goes up, current homeowners have a larger cushion between their property’s value and the money they owe on their home. As a result, they’re more likely to avoid an underwater mortgage. Otherwise called an upside-down mortgage, this home loan has a higher principal than the home’s worth. So, you may have a $200,000 mortgage, but your home value has decreased to $175,000 – you have an underwater mortgage. Thus, this can be a challenge if you’re looking to refinance or sell the property. A higher home value prevents this imbalance. Many homeowners have their property appraised annually to stay on top of their home’s value.

New Construction Trends Are Likely To Be Positive, But High Demand Could Create A Bottleneck

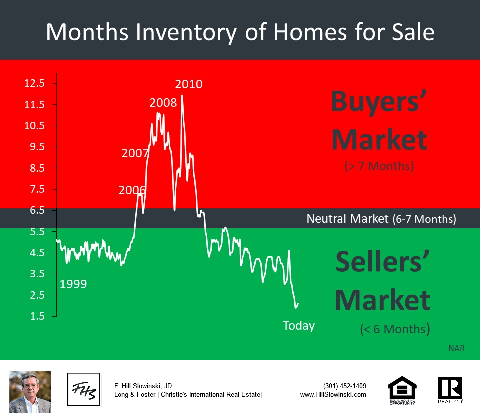

Mortgage rates weren’t the only thing to hit record lows in 2020. Housing inventory, according to REALTOR.com, was also at its lowest. Essentially, there are few homes available to potential buyers. Many are looking to construct new houses instead, mainly because certain areas are in such high demand. However, builders are likely to face bottlenecks in terms of shortages as a result. These shortages include a lack of building materials and even skilled labor, according to the NAHB, or the National Association of Home Builders.

If you are a home buyer looking to build your new home, whether it’s an entirely new construction or a total renovation, you may need a new construction loan. There are several loans, which depend on the borrower and their goals, available. Two examples are a construction-only loan to cover the costs of the actual construction or an owner-builder loan for the home builder with contractor experience. However, high demand for new constructions can drive up costs in the exact same areas the NAHB describes, which will affect how much is necessary to take out in a loan. So, research ahead of time and ensure you have the means to support the loans in this current market.

A Seller’s Market Is Predicted

A seller’s market occurs when supply does not meet demand. So, there are numerous interested buyers, but they’re facing low real estate inventory. December 2020 showcased this downturn in inventory when the National Association of REALTORS reported that inventory was down 22% from the previous year. However, it’s predicted that median sales price will go up by 5.7%, and existing home sales will increase by 7%. This dynamic puts sellers at an advantage and creates an atmosphere for competitive, raised pricing. Even when we see some of these trends begin to normalize this year, as discussed by REALTOR.com, demand will keep those inventory levels relatively low and maintain the seller’s market.

Although sellers will have an advantage, buyers can still negotiate. It’s expected, actually. However, negotiating can be intimidating, so it’s best to work with an agent or REALTOR®. They act as the middleman between you and the seller to make sure your side of the conversation is heard, and you get the most out of the deal that you can or even help you walk away if necessary.

Should We Be Worried About A Crash In 2021?

Due to COVID-19’s impact on the economy and industries, such as housing, it is more than fair to be concerned about drastic future market shifts. You wouldn’t be alone in your concern either. Last year also had its fair share of speculation. The stability of the market depends on consumers’ confidence and the supply/demand ratio. Both of which were affected by the pandemic. So, the situation was a perfect storm of anxieties for sellers and buyers alike. Homeowners were hesitant to list because they were unsure about prices and were concerned about the health of those who might want tours. Even though there was demand, buyers were also insecure because of the economic instability earlier on in 2020.

Still, despite the economic concerns, demand grew. Thus, 2020 avoided a housing market crash, and so it is very likely that 2021 will, too.

However, it’s too simple to just say, “it won’t happen.” There is evidence that tells us why we don’t have to fear another 2008 Great Recession housing bubble burst this year. Foremost, the previous housing crash’s environment around mortgages was different. From 2007 to 2010, the U.S. experienced the subprime mortgage crisis. Essentially, mortgages were turned out to high-risk borrowers. This opened up the market to a greater pool of people, and that drove up house prices. When those prices peaked, mortgage debt rose as well, which led to a collapse on the part of the borrowers and the lenders. Housing prices and the number of buyers shot down, which ended with the real estate market stagnating.

Loan standards have improved since the early 2000s, evident by the declining mortgage credit availability index put out by the MBA. At 122.1 in December 2020, it indicates that standards are tightening. So, the current borrowers are much lower risk than they were before. Also, according to Norada, the recovering economy is a key indicator against a crash. Fannie Mae Economic and Strategic Research (ESR) group, projects the U.S. economy will grow by 5.3% in 2021. The healing economy, plus the previous indicators (low mortgage rates, high home value, and high demand), all point to a stable housing market for the upcoming year.

Keep in mind, however, that world events can influence these outcomes. So, it’s best to stay up to date on global and national news to help predict housing trends.

Looking Back At 2020 Housing Market Predictions: Were They Accurate?

The 2020 Housing Market Predictions had a range of expectations depending on the source. It seems that some of the earlier assessments might have been the most off-base, such as a 2018 press release put out by Zillow. Surveyed real estate experts submitted to a belief that 2020 would feature a housing recession due to monetary policies. Although that may have been wrong, they examined the right pieces, such as the market’s lack of affordability.

As predictions closed in on 2020, there was a smaller margin of error in plotting possible events. Forbes rightfully predicted that mortgage rates and inventory would stay low while prices would rise, though the market’s extremes eluded them. Rocket Homes® predicted similarly and even saw the significant role millennials would play in the year, though also did not know the influence COVID-19 would have on real estate.

However, it’s easy to understand why the older predictions were less likely to pinpoint the flow of events. Even predictions as recent as December 2019 were unaware of the coronavirus and its monumental effects on the market. After all, the coronavirus was not in play at the time that some forecasts were written. It significantly influenced the 2020 housing market but was a surprise. So, even sites that predicted correctly don’t necessarily have the explanation correct. COVID-19 destabilized many aspects of the field itself and experts’ confidence to predict what might happen because it was relatively unprecedented. Yes, they were right that mortgage rates would stay low and inventory would be limited, but that’s because of the highly competitive purchasing seen throughout the 2020 year, rather than just a continuation of typical trends.

Summary

While unexpected events can make predicting market behavior difficult, there are still favorable indicators that it could be a good time for prospective buyers. Mortgage rates will likely stay low throughout 2021, and while rising prices may be an issue for some, there won’t be any extreme spikes. So, both buyers and sellers can expect a relatively consistent field for competitive pricing and negotiation.

The slow stabilizing of the economy promises opportunities for the competitive market. However, COVID-19 has demonstrated that outside forces can quickly affect how people interact with real estate. Furthermore, the aftershocks of the pandemic will continue to shape the housing market. Recovery can be unpredictable sometimes, which can make shopping for your own home difficult during this time. Even with low interest and new build options, it can be intimidating to put your foot in the door. You don’t have to deal with your questions and concerns on your own, though. If you are considering buying a home, contact a mortgage expert. He can work with you to navigate the current real estate market and pursue a home that fits your unique needs.

- By Ashley Kilroy May 15, 2021

- Reprinted from Rocket Mortgage/Quicken Loans,